My Honest Hyperliquid Vaults Review: Results After 1 Month

The decentralized finance (DeFi) landscape is a relentless sea of volatility, promises of high annual percentage rates (APR), and, all too often, hidden risks. In this chaotic environment, Hyperliquid has emerged as a beacon of interest, particularly its localized “Vaults.” For investors holding a spot crypto portfolio, the allure of generating yield that potentially hedges against market downturns is strong.

But how do these vaults actually perform when you put real capital into them? Are the displayed APRs sustainable? How is market volatility handled?

Exactly one month ago, I decided to move beyond theory and launched a personal experiment with an initial investment of approximately $400. My goal was not just to chase maximum yield, but to test a disciplined strategy with a specific focus on risk mitigation.

Here is an honest, unvarnished look at my results, my selection criteria, and the reality of managing a diverse portfolio of Hyperliquid vaults.

The Strategic Blueprint: Goals and Expectations

Before diving into the numbers, it is crucial to understand the context of this experiment. I didn’t enter this randomly. I had specific performance targets and risk thresholds.

My target APR for this investment is 50% annually. While this sounds aggressive compared to traditional finance, in the context of Hyperliquid’s leveraged trading vaults, it is a plausible, though ambitious, objective.

However, yield chasing without a plan is a recipe for disaster. My primary constraint was maximum draw-down (MDD). My target MDD limit is set at 30% for the entire portfolio. This means that at no point am I comfortable losing more than 30% of my principal to gain that targeted yield.

Furthermore, my investment in these vaults serves a specific structural purpose. I use these funds as a protective layer for my spot crypto portfolio. Approximately 2/3 of my strategies in this experiment are market-neutral or defensive, aimed at generating stability when the main market drops. At the same time, 1/3 is directional, designed to capture market alpha when things turn bullish.

Portfolio Construction and Selection Criteria: How I Chose My Vaults

Many users make the mistake of sorting Hyperliquid vaults by the highest displayed APR and simply clicking “Deposit.” My approach was the opposite. I utilized a rigorous, risk-first methodology.

I currently use 8 different vaults, with capital distributed equally among them. This equal-weight distribution minimizes dependency on any single strategy, even though the strategies themselves are vastly different.

When filtering the hundreds of available vaults on Hyperliquid, I relied heavily on four key metrics:

1. Maximum Draw-Down (MDD) – The Primary Filter

The very first metric I look at is the historical MDD. This is the most accurate reflection of the strategy’s risk profile during hostile market conditions.

- My Requirement: The vault’s historical MDD must be below 30%. If a strategy has historically dropped by 50% or 60% (even if it recovered), it does not fit my current risk tolerance for this defensive portfolio. Preferably, I seek strategies with a proven track record of staying below 20%.

2. Vault Age (History) – The “Battle-Tested” Variable

A high APR over one week means almost nothing in DeFi. It could just be a result of one lucky leveraged trade. I needed to see sustainability.

- My Requirement: I only consider vaults that are at least 100 days old (preferably older). The vault must have survived various market cycles—pumps, dumps, and chop—to demonstrate that its strategy can adapt to different regimes.

3. Total Value Locked (TVL) – The Liquidity Question

The size of the vault matters. If a vault has only $10,000 in TVL and I deposit $400, I become a significant percentage of its liquidity, which can negatively affect the strategy’s performance (e.g., higher slippage).

- My Requirement: I prioritize larger TVL vaults. While I did “dilute” my allocation with a few smaller, high-quality vaults because my $400 investment isn’t large enough to move the needle, the backbone of my portfolio is in robust, heavily-capitalized vaults. If my future investment grows, I will move more capital exclusively to higher-TVL strategies.

4. The “Curve Visual” – The Silent Indicator of Quality

Numbers tell one story, but the chart tells another. For me, the visualization of the vault’s performance curve is non-negotiable.

- My Requirement: The curve must be soft and consistently upward-trending. It should look like a smooth staircase, not a rollercoaster. I avoid vaults with sharp, jagged spikes upward, followed by deep, vertical drops. A smooth curve, even without looking at the raw data, signals that the strategy is designed for stable, long-term profit generation, likely with very careful risk management on every trade.

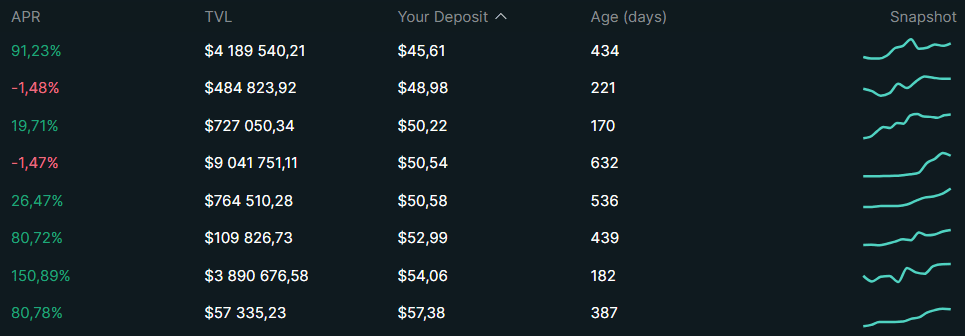

Above is the current list of vaults I use. You can see the differences in their TVL, age, and, most importantly, the smoothness of their return curves. This is the basis of my diversification.

1 Month Results: The Reality Check

We have officially hit the one-month mark of this experiment. My initial investment of approximately $400 has yielded a total profit (PnL) of approximately +$10.

Mathematically, this translates to roughly a 2.5% return for the month. On an annualized basis (projecting forward without compounding), that’s approximately 30% APR.

You might look at my 50% APR target and my current 30% APR projection and feel that this experiment is underperforming. However, performance must always be viewed in relation to risk.

During this first month, the portfolio’s actual maximum drawdown (MDD) was only about 4%. When you compare a 4% actual risk to a 2.5% monthly gain (30% annualized), the risk/reward ratio is excellent. I achieved my stability goals, even if I haven’t yet reached my aggressive income goals. My spot portfolio was safe, and my vault capital grew.

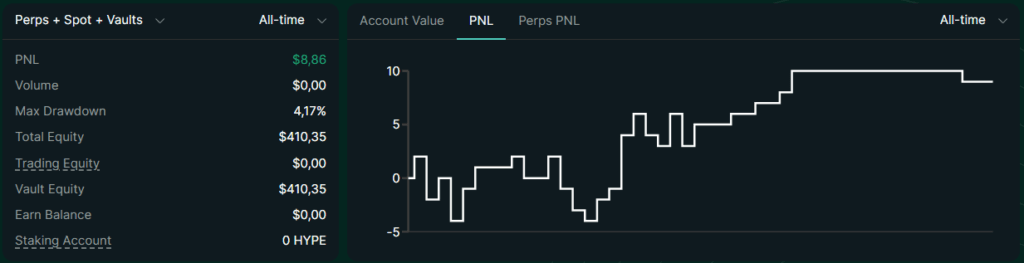

This is a screenshot of my personal Hyperliquid portfolio. You can see the steady performance growth over the last 30 days, and a net profit and loss of about $10.

Challenges and “The Bad News” (What I Learned)

A true “honest review” cannot focus solely on the profits. Managing this diverse vault portfolio this month revealed several significant challenges and operational risks that investors must understand.

1. The Closure and Loss of a Vault

The biggest issue I faced this month was the sudden closure of one of my selected vaults. A vault I had invested in ceased operations unexpectedly. While this was not a catastrophic hack, it created immediate logistical and financial overhead.

- The Impact: The closure and subsequent withdrawal/reallocation process resulted in a -1% loss to the total portfolio’s PnL. This small loss slightly dampened my overall returns and serves as a crucial reminder: You are not just trusting the Hyperliquid protocol; you are trusting the individual strategy owner/operator. When a vault shuts down, you might lose money on transaction fees or timing your entry into a new vault incorrectly.

2. The APR Paradox: A Misleading Projection

When you browse Hyperliquid, the displayed “APR” for a vault is usually a projection based on its recent short-term performance. This is perhaps the most dangerous trap for new users.

- The Problem: The current APR projection might represent a massive profit spike from yesterday’s crypto pump. It rarely accurately predicts the next 30, 90, or 365 days.

- My Learning: Over a longer duration, the data based solely on the displayed APR becomes incorrect or irrelevant. To truly understand a vault’s health, you cannot rely on the main screen. I have learned that I must manually click into each specific vault and review its daily historical performance data to get a realistic picture of its sustainable average return.

Active Management: Rebalancing and Re-entry Strategies

One of the main takeaways from this first month is that Hyperliquid vaults are not a “set it and forget it” investment, especially when using multiple vaults. I must maintain a proactive approach.

I am not simply holding these 8 vaults indefinitely. I have implemented specific rebalancing rules:

- Rebalancing on Profits: In the case where any individual vault’s performance increases the allocation value by +50% (making it “overweight” in my portfolio), I will rebalance. I will withdraw the profits and redistribute that capital across my other 7 vaults, keeping the portfolio equally weighted.

- Exiting on Loss (Stop Loss): My capital distribution is important. If any single vault experiences a significant drawdown of -30%, I will take an active stop-loss and exit that vault completely. I will re-evaluate the strategy, wait for a potential recovery (as an observer), or, more likely, reallocate that capital to a new vault that fits my entry criteria.

Conclusion and Outlook: Entering Month 2

After one month, I view this Hyperliquid experiment as a tactical success. My capital is safe (only 4% MDD), and I am in profit (+2.5% month over month) despite the market’s constant chop.

Crucially, my primary goal of providing a defensive layer for my spot portfolio has been achieved. When my spot portfolio fluctuated wildly, my vault portfolio remained largely stable, and that is worth the operational complexity of managing 8 different strategies.

However, the road to 50% APR with 30% MDD tolerance is difficult. I cannot relax my vigilance. In the coming month, I will be focused on:

- Manual Data Verification: Moving beyond the displayed APR and deep-diving into individual vault data to find a replacement for the closed vault.

- Rigorous Rebalancing: Adhering strictly to my +50%/-30% rules to maintain my 2/3 defensive and 1/3 directional allocation balance.