REITs or Rentals? The Truth About Liquidity and Tax Benefits

In the real estate landscape of 2026, the choice between Real Estate Investment Trusts (REITs) and Physical Rental Properties is no longer a matter of declaring a definitive winner. Instead, it is a strategic decision dictated by your liquid capital requirements, time horizon, and tax architecture. With global real estate allocations projected to rise by 15% year-over-year, both paths offer distinct, high-powered mechanisms for an ambitious empire builder.

While public REITs deliver the friction-free transaction speeds of the modern stock market, direct physical rentals provide unmatched tax shelter capabilities. Direct real estate remains a premier wealth-preservation asset class because of its ability to legally mitigate income tax liabilities.

1. Liquidity: The “Speed of Cash” Gap

Liquidity defines how quickly an asset can be converted back into sovereign cash without absorbing a devastating haircut to its intrinsic value. In 2026, the delta between liquid paper real estate and illiquid brick-and-mortar property is wider than ever.

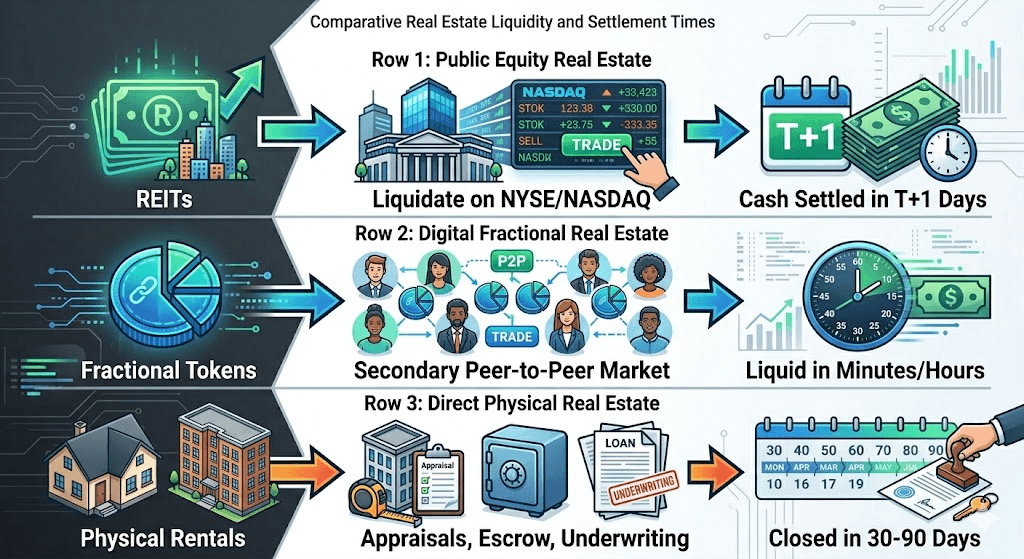

Public REITs: High Liquidity

Publicly traded REITs (such as warehouse giant Prologis or digital infrastructure specialist American Tower) function exactly like public equities. They trade on major exchanges like the NYSE and NASDAQ. If an investor needs to reallocate $100,000, they can execute a market or limit order within seconds during standard trading hours. Under current clearing guidelines, capital is settled and completely fluid within one to two business days.

Physical Rentals: Low Liquidity

Directly owned property is inherently rigid. Disposing of a physical multifamily or single-family asset requires an average of 30 to 90 days to finalize. This timeline is bound by structural underwriting, property appraisals, environmental inspections, and bank financing approvals. Furthermore, transaction friction is remarkably high. When factoring in brokerage commissions, title insurance, legal fees, and transfer taxes, transaction costs routinely consume 6% to 10% of your hard-earned equity.

Tokenized Alternatives

For investors demanding a middle ground, fractional tokenization platforms are fundamentally transforming this liquidity curve. Utilizing blockchain architecture, Lofty allows individuals to buy fractionalized, compliant equity tokens of specific cash-flowing single-family homes.

Unlike traditional fractional syndications that impose multi-year holding periods or rigid “Redemption Gates,” Lofty features a highly active peer-to-peer secondary market. This allows token holders to list and liquidate their real estate equity fractions almost instantly to an international pool of buyers, completely neutralizing the multi-month closing process associated with physical property.

2. Tax Benefits: The Wealth-Building Engine

Tax efficiency is the exact domain where direct physical real estate investments structurally outperform traditional public REITs, making direct ownership a primary tool for high earners looking to shield their income.

| Tax Feature | Public REITs (Passive Paper) | Physical Rental Properties (Direct/Active) |

| Depreciation Treatment | Absorbed at the corporate level; you receive net cash distributions. | Generates non-cash “Paper Losses” to directly offset net rental distributions and active income. |

| Dividend/Income Taxation | Typically taxed as Ordinary Income (up to 37% marginal rates). | Rental income can be offset entirely by depreciation, resulting in 0% effective tax rates. |

| Capital Gains Mitigation | None. Capital gains taxes are triggered immediately upon selling shares. | 1031 Exchange Elimination: Unlimited tax deferral by rolling equity into a replacement property. |

| Section 199A QBI Deduction | Pass-through 20% deduction on qualified REIT dividends. | 20% deduction available if the portfolio satisfies “Trade or Business” legal standards. |

The Depreciation Trap (The Good Kind)

When you own physical real estate, the IRS permits you to artificially “depreciate” the structural value of the residential property over a fixed 27.5-year timeline. This non-cash accounting expense often creates a net loss on paper, even when the property is generating substantial positive cash flow.

Taxable Rental Income = Gross Rent – Mortgage Interest – Operating Expenses – Depreciation

For example, a property could easily deposit $1,000 per month in clean net cash flow into your bank account while showing a technical loss on Schedule E. This paper loss shields your distributions from tax and can occasionally offset ordinary W-2 income if you qualify as a Real Estate Professional.

Public REIT Tax Reality

Conversely, public REIT dividends are structurally disadvantaged. Because a REIT must distribute 90% of its taxable income to shareholders to maintain its corporate tax exemption, the IRS treats these payouts as “Unqualified Dividends.” Consequently, they are taxed at your highest marginal ordinary income tax bracket.

With the current top federal marginal bracket resting firmly at 37%, wealthy investors face significant tax drag on their REIT returns. While the Qualified Business Income (QBI) deduction offers a helpful 20% pass-through reduction, the effective tax rate on a public REIT dividend stream remains significantly higher than the optimized, near-zero tax environment of an engineered physical rental portfolio.

3. Leverage: Why Physical Rentals Scale Faster

The primary reason direct real estate investments scale quickly is the accessibility of non-recourse and conventional long-term leverage. While investment property mortgage rates maintain a baseline range of 6.5% to 7.5%, the underlying math of leverage drastically amplifies cash-on-cash performance.

Consider a standard capitalization comparison:

- The Rental Scenario: You deploy $50,000 as a 20% down payment to purchase a $250,000 residential asset. If the local housing market experiences a modest 5% market appreciation, the entirety of the asset grows by $12,500. Because your initial capital allocation was only $50,000, your localized cash-on-cash return scales to an impressive 25% (excluding principal paydown and net rental yields).

- The REIT Scenario: If you purchase $50,000 worth of public REIT shares via a standard brokerage account, you typically deploy 100% cash. If the underlying REIT assets appreciate by 5%, your personal equity grows by exactly 5% ($2,500).

While the corporate entity inside the REIT utilizes institutional debt on its balance sheet, you, as the retail shareholder, do not reap the same exponential wealth acceleration that personal, direct down-payment leverage provides.

4. Top Real Estate Platforms for 2026

If you want to capitalize on real estate yields without managing repairs, dealing with tenants, or handling late-night maintenance calls, specialized alternative platforms offer compelling alternatives.

Fundrise

Fundrise remains a highly versatile option for retail diversification. With an accessible $10 minimum baseline, the platform aggregates retail capital into a network of proprietary “eREITs” and private funds. It primarily targets institutional-grade multifamily apartment complexes, industrial logistics infrastructure, and single-family build-to-rent communities, emphasizing steady income alongside long-term capital appreciation.

Arrived

Arrived has established a clear stronghold in the fractional single-family rental and vacation property sectors. It enables individual investors to buy shares in specific residential assets for as little as $100. Arrived completely manages property operations, handles tenant placement, and oversees asset maintenance while distributing net rental dividends to investors quarterly.

Lofty

For forward-thinking investors seeking maximum flexibility, Lofty is a premier solution for tokenized real estate. By fractionalizing direct rental properties into compliant digital assets on the blockchain, Lofty eliminates the traditional liquidity penalties of real estate investing. Investors earn rent paid out daily and can buy or sell their property fractions seamlessly on the secondary marketplace with zero lock-up constraints, bypassing the multi-month closing delays of conventional transactions.

RealtyMogul

RealtyMogul caters to accredited and high-net-worth investors seeking direct access to institutional commercial real estate (CRE). Requiring elevated entry minimums (frequently $5,000 to $15,000+), the platform permits individuals to co-invest alongside institutional sponsors in institutional assets, including Class-A office towers, localized medical campuses, and anchored retail shopping centers.

Conclusion: Designing Your Allocation Strategy

Choosing between REITs and physical rentals requires aligning your investment strategy with your financial goals. If your objective is capital agility, passive diversification, and immediate cash availability, public REITs or fractional real estate vehicles are ideal choices.

However, if your primary goal is tax minimization, equity compounding via long-term leverage, and multi-generational wealth preservation, direct physical ownership remains unmatched. Utilizing a hybrid strategy—combining liquid public REITs inside tax-advantaged retirement accounts with fractional, cash-flowing tokenized assets via Lofty—allows you to build a resilient real estate portfolio tailored for both continuous cash flow and long-term tax efficiency.

FAQ

What is the practical application of the “1% Rule” in today’s market?

The 1% Rule states that the gross monthly rental income of a physical property should equal or exceed 1% of its total acquisition price. In the current elevated asset valuation environment, finding an investment that meets this criterion is exceptionally rare in primary metropolitan regions. However, it serves as a reliable metric to identify high-yield cash-flowing opportunities in secondary and tertiary markets.

Do I have to pay taxes on REIT dividends if they are held inside an IRA?

No. If public REIT positions are held inside a tax-sheltered account like a Roth IRA, your distributed dividends and eventual capital gains are completely tax-exempt. Holding REITs in an ordinary brokerage account triggers high marginal income tax rates, so utilizing a Roth IRA is an effective strategy to maximize your net returns.

What is the dynamic known as “Phantom Income”?

Phantom Income refers to a tax liability where an investor is taxed on their proportional share of a partnership’s or pass-through entity’s generated net profits, even if the entity did not distribute physical cash to the investor. Publicly traded REITs avoid this issue by law, as they are contractually required to distribute 90% of their taxable income directly to shareholders annually.

Can I realistically manage a direct rental property myself?

Yes, you can manage rentals independently, though standard property management companies typically charge 8% to 12% of gross rental revenue to oversee operations. Many independent landlords now use modern property management software like Baselane, Stessa, or Hemlane to automate background checks, generate leases, track bookkeeping, and collect rent at minimal cost.

Which real estate vehicle offers superior long-term inflation protection?

Both asset structures offer excellent inflation defense, as real estate operates as a classic “hard asset.” When inflation rises, landlords can adjust lease rates upward, while the replacement cost of the physical properties increases. Public REITs pass these adjustments along via expanding dividend yields, while physical rentals capture the upside through increasing cash flow and rising property values.