The Kelly Criterion for Traders: How to Mathematically Maximize Your Edge

The transition of the Kelly Criterion from a niche mid-century gambling formula to a core structural feature of institutional-grade algorithmic trading platforms represents a fundamental shift in how modern financial markets are navigated. For decades, retail market participants focused almost exclusively on directional prediction—debating whether an asset would move up or down, parsing technical indicators, or relying on fundamental narratives to determine market entry. In contrast, institutional risk managers recognized early on that predictive accuracy is only a minor fraction of long-term survival. The far more critical component of a sustainable trading edge is position sizing.

As we progress through the volatile financial ecosystem of twenty twenty-six, relying on arbitrary percentages, emotional conviction, or rigid fixed-dollar sizing is an absolute recipe for operational ruin. The modern trading environment requires a rigorous, mathematically sound allocation engine that systematically balances the pursuit of geometric growth against the constant threat of capital destruction. The Kelly Criterion provides exactly that engine, calculating the precise fraction of your available capital to risk on any single market confrontation to maximize your long-term compounding rate.

1. The Core Architecture: Understanding Edge versus Odds

To effectively implement the Kelly Criterion within a modern systematic portfolio, an operator must completely understand the distinct relationship between an operational edge and payout odds. The framework is not designed to find high-probability setups or discover hidden market trends; it is engineered to optimize the distribution of capital across an existing, historically verified trading edge.

The traditional formula deployed by quantitative desks strips away subjective human bias by evaluating two explicit structural inputs: your verified probability of winning and your real-world reward-to-risk payout ratio. The probability of winning represents the historical or calculated frequency with which your strategy successfully captures a profit target under a given set of market parameters. The payout ratio defines the average magnitude of your winning trade allocations relative to the average magnitude of your losing trade allocations.

When balanced against one another, these two data points yield a mathematical suggestion of exactly how much risk exposure your equity curve can absorb. If a strategy exhibits a high win rate but a minimal payout ratio, the formula scales down the appropriate position size to insulate the account from a sudden string of small losses that could easily erase multiple wins. Conversely, if a systematic model captures massive geometric profits on a relatively low win rate, the formula calculates an optimized size that allows the trader to survive a prolonged series of consecutive losses before capitalizing on the inevitable high-payout winner.

The Modern Reality: Why Full Kelly Sizing is an Operational Trap

While the theoretical mathematical foundations of full-scale Kelly execution promise the absolute fastest path to capital compounding, applying the raw, unadjusted Kelly recommendation in a live electronic marketplace is a dangerous trap that frequently results in severe, irreversible account drawdowns. Full Kelly sizing relies on an assumption that your statistical measurements of win rates and payout ratios are perfectly accurate and completely static across time. In reality, modern financial markets are characterized by continuous regime shifts, structural liquidity gaps, sudden data revisions, and unexpected black swan events.

If your historical performance metrics are even slightly miscalculated—or if a sudden shift in macroeconomic policy causes your edge to decay—executing full-scale Kelly calculations will systematically over-allocate capital to a failing strategy. A string of just five or six consecutive losses under a full Kelly allocation model can easily trigger an equity drawdown of fifty to seventy percent. Rebounding from a drawdown of that magnitude requires a subsequent geometric return that very few individual systems or human operators can ever hope to achieve.

Because of this inherent vulnerability, professional proprietary desks and systematic asset managers across global markets enforce strict allocation dampening techniques. Instead of deploying full-scale calculations, professional operators utilize a fractional implementation framework, with half-intensity or quarter-intensity models serving as the industry baseline.

- The Half-Kelly Calibration: By taking exactly fifty percent of the mathematically calculated Kelly fraction, an operator can capture roughly seventy-one percent of the maximum theoretical compounding rate of the full strategy while simultaneously reducing overall portfolio volatility by approximately sixty-two percent.

- The Quarter-Kelly Calibration: Scaling the allocation down to twenty-five percent of the formula’s output serves as an exceptional structural shield for conservative long-term capital allocators. It provides a massive safety buffer against human analytical errors, structural execution slippage, and unexpected volatility expansions, eliminating the realistic mathematical probability of experiencing a ruin event.

2. Infrastructure: Premier Technical Venues for Automation

Executing complex risk-modeling algorithms on a scratchpad or via manually updated spreadsheets is entirely obsolete in twenty twenty-six. High-velocity trading platforms have natively integrated specialized capital allocation engines into their core technical environments, enabling systematic traders to automate their position sizing based on real-time trailing performance data.

Interactive Brokers

Interactive Brokers remains an industry standard for multi-asset institutional operators through its advanced Portfolio Analyst suite and updated Trader Workstation terminal. The platform features dedicated risk-constrained allocation algorithms within its specialized quantitative module. Rather than requiring the manual entry of static performance variables, the system actively audits your trailing one hundred completed trade executions to compute your real-world win rates and payout ratios dynamically.

When prepping an order block for highly volatile assets like equities or global commodity futures, the algorithmic module automatically determines the appropriate contract size based on your verified performance parameters. Furthermore, the updated quantitative environment accounts for structural correlations across your entire portfolio. If you attempt to initiate a long position in a high-beta technology asset while already holding an active long exposure in a highly correlated digital or precious metal market, the system automatically scales down the calculated position size. It recognizes that both instruments frequently move in tandem with broader macro sentiment shifts, preventing dangerous accidental exposure concentrations.

TradingView

For visual systematic traders, TradingView’s Pine Script development environment offers a highly flexible canvas for implementing automated sizing logic. The platform supports community-engineered and custom indicators that seamlessly map quantitative allocation suggestions directly onto live charting interfaces. When an operator identifies a potential technical setup, the script scans the underlying asset’s historical average true range over a specific rolling period to determine the structural volatility environment.

By cross-referencing this localized volatility data with the trader’s historical performance metrics, the charting engine projects a recommended position size directly onto the execution candle. This allows users to view their optimal financial risk limits before an order is ever routed. This framework is tied directly into deep backtesting engines, allowing developers to execute comprehensive multi-year historical simulations that compare the precise performance of an identical technical script under standard fixed-percentage risk models versus dynamic fractional allocation systems.

Tastytrade

Tastytrade is engineered from the ground up for mathematically driven options practitioners who require a granular focus on systemic probabilities and implied volatility metrics. The platform centers its entire execution interface around a dynamic probability of profit overlay, moving completely away from traditional linear pricing charts to highlight real-time statistical distributions.

The software automatically tracks complex mathematical Greeks to determine the precise probability of a specific option’s configuration finishing in the money at expiration. This real-time probability metric can be plugged directly into the system’s integrated position sizing modules. By ensuring that large premium collection strategies or low-probability directional options plays are sized in strict accordance with their underlying mathematical expectancy, the platform prevents retail options operators from over-allocating capital to low-probability directional plays that frequently look appealing but present an unhedged threat to core capital balances.

QuantConnect

QuantConnect provides an institutional-grade cloud architecture tailored explicitly for algorithmic developers and quantitative coders utilizing the proprietary LEAN engine. The platform offers native libraries dedicated entirely to the deployment of automated capital allocation models. When designing a fully automated trading bot, developers can configure the system to actively track the model’s trailing thirty-day performance metrics.

If the script enters a period of structural decay or encounters a highly adverse market regime, the cloud execution engine automatically contracts the system’s maximum leverage allowances and downsizes individual order block volumes. Conversely, when the system enters a highly favorable market regime where actual win rates align perfectly with historical expectations, the allocation engine scales up position sizes toward your predefined fractional cap, ensuring maximum compounding efficiency without requiring manual oversight.

3. The Execution Blueprint: Implementing the Allocation Checklist

To safely and effectively transition your existing investment strategy into a mathematically optimized framework, you must run every prospective position through a rigid validation sequence.

Phase 1: Establish Your Statistical Edge

You must compile a minimum of twelve months of verified trading data to calculate your authentic baseline win rate. If your data demonstrates that you successfully close fifty-five out of every one hundred executed trades with a net profit, your statistical baseline value is zero point fifty-five. You must avoid using theoretical backtested win rates that have not been exposed to the raw emotional friction and structural execution slippage of a live market environment.

Phase 2: Compute Your Payout Odds

Analyze your historical performance data to determine the precise ratio between your average profitable trade and your average losing trade. If your trailing metrics show that your average winning transaction yields one thousand dollars while your average losing transaction results in a loss of five hundred dollars, your real-world payout factor is exactly two.

Phase 3: Calibrate the Fractional Multiplier

Once your baseline inputs are established, process them through the core formula to calculate your theoretical full allocation limit. If the raw mathematical output suggests risking ten percent of your master account equity on an upcoming execution, you must immediately apply an institutional safety multiplier based on your personal risk tolerance. Conservative allocators routinely apply a quarter-intensity rule, reducing that ten percent theoretical recommendation to a highly stable and defensible three percent operational risk model.

Phase 4: Enforce an Absolute Hard Cap

The financial markets of twenty-twenty-six are highly non-linear systems prone to extreme liquidity dislocations and systemic shocks. Even when a highly optimized algorithmic model identifies a theoretically flawless setup with massive positive mathematical expectancy, you must enforce a hard structural cap on your maximum portfolio exposure. Maintaining a strict upper allocation boundary between fifteen and twenty percent of total master equity on any individual position protects your enterprise capital from unexpected black swan events that can easily bypass standard stop-loss orders through extreme overnight exchange gapping.

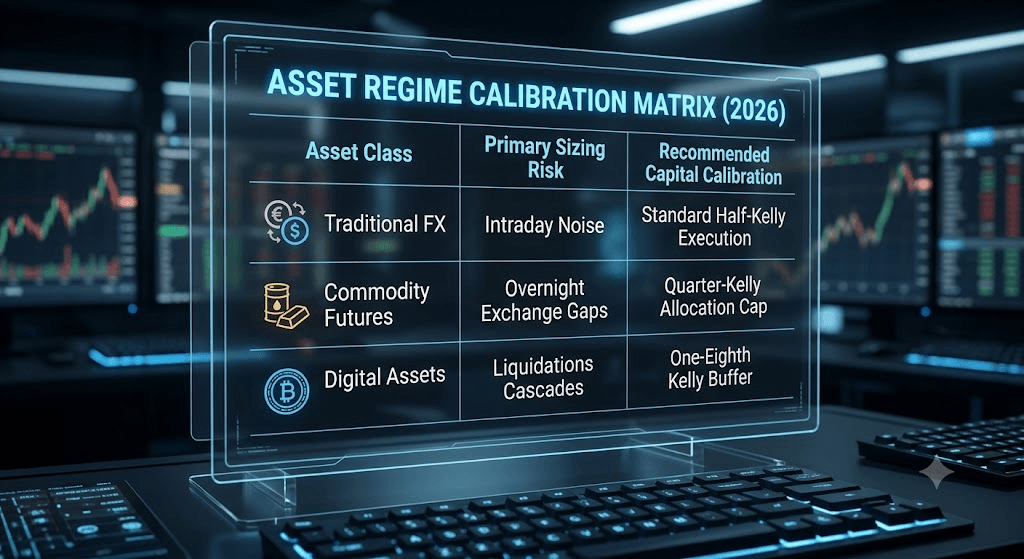

4. Operational Adjustments Across Traditional & Alternative Asset Classes

Implementing a dynamic mathematical position sizing model requires deep adaptation based on the specific asset class you are executing across. The underlying liquidity profiles, settlement mechanisms, and structural volatility characteristics of different financial instruments demand highly customized risk profiles.

Navigating Spot and Derivatives via Professional Brokerage Frameworks

For systematic operators managing diverse portfolios centered around traditional macro foreign exchange pairs, global stock indices, and traditional commodity contracts, routing execution through a highly capitalized institutional broker like RoboForex provides a vital structural advantage. Utilizing their high-speed MetaTrader 5 execution environment allows programmatic traders to implement genetic optimization sweeps that stress-test dynamic sizing scripts across decades of premium liquidity data.

Because traditional contract and foreign exchange markets exhibit structural mean-reverting tendencies punctuated by clear macroeconomic trends, strategies executed in these spaces can typically support standard half-intensity or quarter-intensity allocations. The presence of multi-threaded execution servers ensures that as your trailing win rates fluctuate in response to central bank interventions or interest rate revisions, your position sizes adapt instantaneously, shielding your master account from the operational drag of manual recalculations.

Managing Extreme Volatility Streams within Digital Asset Ecosystems

When transitioning a systematic position sizing model into the highly fragmented and volatile digital asset markets, the baseline risk configuration must be recalibrated to account for hyper-exponential price movements and regular liquidity liquidations. Programmatic traders executing models through cloud-native automation infrastructures like Bybit must recognize that digital asset regimes are uniquely prone to structural leverage flushes, where billions of dollars in open interest can be wiped clean from the order books in a matter of minutes.

In these environments, utilizing standard full or even half-intensity allocation calculations is exceptionally dangerous. High-velocity asset drops can easily gap past digital stop-loss parameters, leading to severe execution slippage that breaks your mathematical modeling.

Therefore, when deploying automated strategies through advanced derivative platforms like Bybit, quantitative developers routinely implement a hyper-conservative one-eighth intensity configuration. This highly restricted allocation framework allows an automated bot to absorb extreme intraday volatility spikes and survive severe liquidations without triggering a systemic ruin event, while safely capturing the massive geometric trend runs that characterize digital asset expansions.

FAQ

What specific operational action must be taken if the mathematical output is negative?

If processing your performance variables through the formula yields a negative numerical result, it indicates that your strategy possesses a negative mathematical expectancy under current conditions. The underlying market edge is held entirely by the exchange or your counterparty, meaning that executing any trades under those parameters will result in a statistical erosion of capital. You must immediately stop execution, bench the strategy, and redesign your core technical parameters.

Is it effective to apply a dynamic position sizing model to long-term physical asset holdings?

No, it is highly ineffective. The framework is engineered explicitly for a sequential series of independent trades where capital is regularly rotated and exposed to explicit win-and-loss outcomes. For passive, long-term asset structures—such as deep physical gold allocations or traditional buy-and-hold real estate indices—a fixed structural asset allocation framework is vastly superior, as you are not actively exiting positions based on a trailing short-term probability matrix.

How can modern artificial intelligence models enhance position sizing strategies?

Advanced machine learning models can be used to scan broader macroeconomic volatility regimes in real time. If an artificial intelligence engine identifies that a specific market is transitioning from a compressed, low-volatility state into a highly erratic, high-velocity regime, it can automatically adjust your historical input expectations downward. By proactively dampening your baseline assumptions before an actual string of losses occurs, the intelligence layer protects your capital base from entering an unexpected drawdown period.

What is the precise definition of the Risk of Ruin metric?

The Risk of Ruin is a definite mathematical calculation that defines the exact probability that an active portfolio will encounter a sequence of negative outcomes severe enough to completely wipe out its capital base. When utilizing unadjusted full allocations, your statistical risk of ruin rises exponentially during periods of performance drift or execution errors. Implementing a disciplined fractional framework forces the mathematical risk of ruin down to near-zero percent across a statistically significant series of trades.

Can dynamic allocation calculations be used safely for options-selling strategies?

Yes, but the inputs must be heavily modified to account for the asymmetric risk profile of option credit strategies. Selling options typically involves an exceptionally high win rate balanced against a very large potential downside if a short strike is breached. If you plug a ninety percent win rate into the formula without enforcing absolute hard limits on your potential loss metrics, the system will suggest an aggressively large position size that can cause sudden liquidation during an extreme tail-risk market expansion. Option sellers must always use a highly conservative fractional multiplier and hard cap individual exposures..