The Risk Management Secret: How to Protect Your Capital Now

Investing is often described as the pursuit of maximizing returns, but for professionals, it is more accurately defined as the systematic management of risk. As we navigate the complex market environment of 2026, traditional asset-allocation safety nets—such as the classic 60/40 stock-bond split—are failing to provide the structural protection they historically did.

In a macroeconomic landscape shaped by persistent inflation and elevated baseline interest rates, the absolute “secret” to protecting capital is no longer about trying to avoid losses entirely. Instead, it relies on the mathematical precision of position sizing and the strategic containment of uncorrelated assets.

The most dangerous phrase in any operator’s vocabulary is “high conviction.” Conviction without a quantitative risk framework is simply gambling.

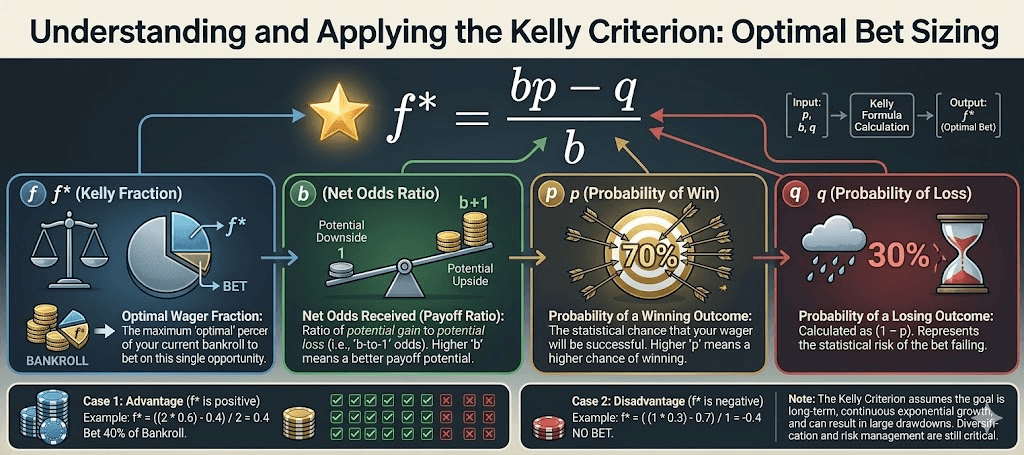

1. The Mathematics of Survival: The Kelly Criterion

The baseline of institutional risk management lies in the Kelly Criterion. Originally developed at Bell Labs, this formula determines the mathematically optimal size of an enterprise position based on your verifiable probability of success and the corresponding potential payoff ratio:

For a professional allocator, the fundamental goal is not to be correct on 100% of execution setups, but to guarantee that a single sequence of failures cannot trigger a ruin event (complete capital liquidation).

In early January 2026, a wave of retail participants was caught completely off guard by a swift 15% structural drawdown across dominant AI infrastructure equities like NVIDIA (NVDA) and ARM Holdings. Traders utilizing aggressive, uncalibrated leverage immediately faced catastrophic margin calls.

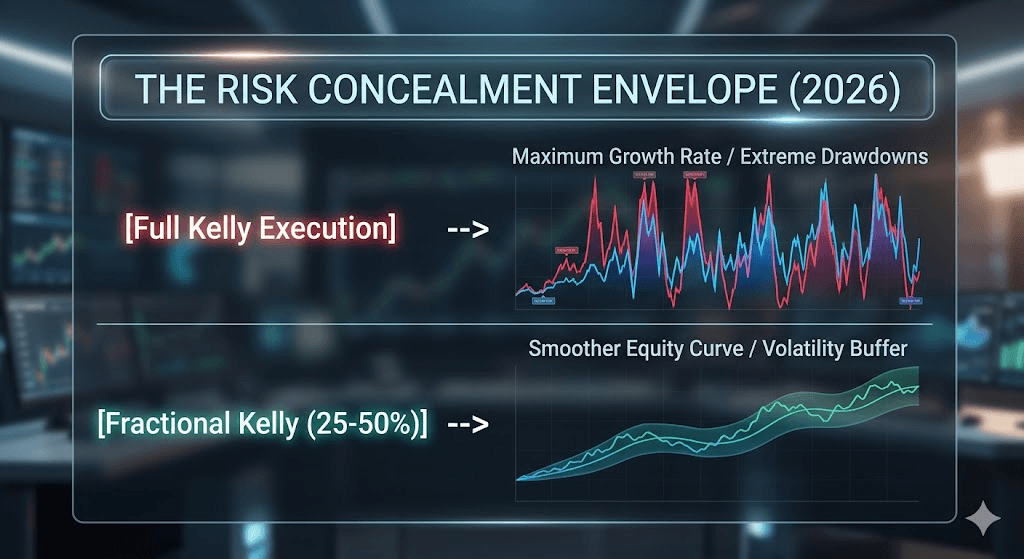

In contrast, systematic portfolios deployed via a “Fractional Kelly” layout—risking only 25% to 50% of the mathematically suggested formula volume—easily preserved their core equity base. By purposefully scaling down the operational allocation fraction ($f^*$), they swapped a marginal degree of theoretical growth for an exceptionally smooth, defensible equity curve.

2. Tail-Risk Hedging: Sourcing “Black Swan” Insurance

Professional capital preservation requires the integration of convex payouts—specialized defense allocations designed to yield massive exponential returns during rare, highly destructive market anomalies. In 2026, Tail-Risk Hedging (TRH) has shifted from an exotic quantitative approach to a standard operational rule for multi-family offices and institutional desks.

Consider the severe market dislocation caused by the sudden April 2025 global tariff shocks. While the broader S&P 500 index (SPY) suffered aggressive liquidations, diversified portfolios carrying a disciplined 1% to 3% structural allocation in deep out-of-the-money Long Put Options or convex tail-risk vehicles like the Cambria Tail Risk ETF (TAIL) watched those specific insurance segments spike by over 300%. This inverse volatility cushion acts as a vital circuit breaker, shielding the investor’s emotional state and preventing them from panic-selling their long-term compound assets at the absolute floor of a market correction.

3. Cash as a Tactical Weapon

In a high-interest-rate regime, the traditional “opportunity cost” of maintaining deep cash positions drops to its lowest relative level in two decades. With 3-month U.S. Treasury bills and institutional money market instruments (such as the Vanguard Cash Reserves Federal Money Market Fund – VMFXX) securely yielding over 4.5%, cash can no longer be dismissed as a dragging asset.

Sophisticated asset managers treat cash as an active, high-optionality tool. Maintaining a structural 15% to 20% liquid capital baseline via accessible short-duration short-term Treasury ETFs like SGOV or BIL shifts an investor’s role from a victim of volatility to a predatory buyer. When sentiment-driven algorithmic sell-offs sweep through the exchanges, the liquid investor commands immediate purchasing power, allowing them to accumulate premier, mispriced companies at steep fundamental discounts while fully invested accounts are forced to remain passive observers.

4. Fundamental Audit: Isolating Value from Hype

The real secret to protecting wealth is acknowledging that risk isn’t merely the fluctuating numbers on your daily monitor; it is the permanent loss of structural purchasing power through poor asset selection.

To systematically separate durable fundamental value from transient market hype, investors deploy advanced analytical toolsets like Tykr to instantly assess an asset’s underlying margin of safety.

- Execute a Margin of Safety Audit: Quantitative Calculation.

Process the target company’s trailing financial reports through an algorithmic valuation engine to verify if the asset is trading at a discount (“On Sale”) or trading at a speculative premium (“Overpriced”).

2. Verify the Structural Score Metrics: Financial Health Check.

Cross-examine the enterprise’s debt-to-equity ratios, free cash flow consistency, and operational return on invested capital (ROIC). A high-scoring profile indicates structural resilience against macro contractions.

3. Deploy Fractional Capital Allotments: Strategic Buffer.

Once an asset is confirmed as fundamentally sound and undervalued, apply your calibrated Fractional Kelly matrix to determine the exact cash allocation, preserving your liquid tactical powder.

FAQ

What is the functional purpose behind a “Fractional Kelly” framework?

A Fractional Kelly system intentionally applies a specific multiplier (such as 0.25 or 0.50) to the position size suggested by the raw Kelly equation. This provides an essential buffer against the natural human tendency to over-estimate trade win probabilities, while drastically dampening the steep portfolio volatility and peak-to-trough drawdowns associated with full-scale Kelly execution.

Is Tail-Risk Hedging an expensive drag on long-term performance?

Yes, tail-risk hedging functions exactly like a premium on an insurance policy. It typically commands an annual budgetary allocation of 1% to 2% of total portfolio equity. During sustained, low-volatility bull markets, this premium represents an explicit drag on net performance, which is the necessary cost accepted to ensure the master portfolio against systemic downside events.

Why is an absolute focus on Uncorrelated Assets mandatory during market panics?

During severe systemic liquidations, traditional asset classes frequently experience a convergence of correlation toward 1.0, meaning almost everything drops simultaneously. Securing truly uncorrelated assets (such as short-duration bills, inverse derivatives, or managed futures) provides a non-liquidating structural component that remains flat or gains value, delivering the urgent liquidity needed to rebalance into discounted risk equities.

What is the premier mechanism for holding cash, “Dry Powder,” right now?

Institutional allocators heavily favor ultra-short Treasury ETFs, such as the iShares 0-3 Month Treasury Bond ETF (SGOV). These instruments offer near-instantaneous cash liquidity on active exchanges while capturing institutional yields north of 4.5%, completely mitigating the systemic credit risks associated with standard banking deposits.