The Truth About Crowdfunding: Why Your ROI Has Strict Limits

In the financial ecosystem of 2026, crowdfunding and Peer-to-Peer (P2P) lending have completely matured into multi-billion-dollar staples of the alternative investment universe. Marketing slogans across the internet regularly dazzle retail investors, promising “effortless, double-digit passive income” and an escape from stock market volatility.

However, professional wealth builders approach these claims with a heavy dose of skepticism. The reality is that your true Return on Investment (ROI) in crowdfunding is ruthlessly capped by a series of structural, regulatory, and mathematical limits. Understanding these invisible barriers is the exact line of demarcation between building a sustainable financial empire and suffering a catastrophic portfolio wipeout.

1. The Ceiling of Risk-Adjusted Returns

As we progress through 2026, the global crowdfunding and alternative debt marketplace is expanding toward an estimated baseline value of $18.5 billion. If you scroll through prominent European P2P hubs like Mintos or PeerBerry, you will routinely see gross interest rates advertised anywhere from 10% to 15%.

The fundamental trap for beginners is treating these headline interest rates as net yields. The first, and most unyielding, limit on your ROI is the Cost of Risk.

The Mathematical Erosion

Even within a highly robust, expanding economy, the baseline default rate for unsecured consumer or small-business P2P loans historically trends around 3% to 4%. When a borrower defaults, a portion of your principal evaporates.

$$\text{Net ROI} = \text{Gross Interest Rate} – \text{Default Rate} – \text{Platform Management Fees}$$

When you apply this math—subtracting localized defaults along with the standard 1% to 2% internal management and servicing fees charged by the platform—that shiny “12% return” is quickly ground down to a modest 6% to 7% net gain. This is an ironclad mathematical ceiling: you cannot consistently harvest equity-like returns of 15% to 20% in unsecured debt without exposing your capital to junk-bond levels of default risk, where the probability of sudden principal destruction skyrockets past 50%.

2. Specialized Platforms and Their Built-In “Niche” Limits

To counter the low yields of unsecured consumer debt, the smart money in 2026 has rotated toward specialized, asset-backed crowdfunding niches. While these platforms provide significantly higher structural safety, they each contain unique, built-in limits on your potential ROI upside.

Discounted Debt Exploitation: Indemo

A rapidly expanding name in the 2026 European fintech landscape is Indemo, which focuses on a highly specialized asset class: Discounted Debt Investments. Indemo allows retail individuals to fractionalize investments into pools of non-performing bank mortgages at a deep discount, aiming for gross targeted returns of 12% to 15%.

The strict limit here is entirely dictated by the Liquidation Value of the underlying real estate collateral (typically located in Spain or Portugal). While buying a mortgage note at a discount provides a massive cushion, if the local Mediterranean housing market experiences a localized 10% price correction, or if the court-ordered foreclosure process stalls, your projected 15% yield will be rapidly consumed by protracted cross-border legal fees and recovery costs.

Rigid Protections: EstateGuru

EstateGuru remains an industry giant for short-term, property-backed bridge and development loans. The platform aggressively mitigates risk by capping its Loan-to-Value (LTV) ratios at 60% to 70%.

While this strict LTV shield provides an exceptional safety net for your principal if a developer defaults, it acts as a permanent ceiling on your wealth accumulation. Because you are purely acting as the debt provider, you capture 0% of the upside if the underlying development doubles in value. You are permanently boxed into your fixed interest rate while the developer extracts the true entrepreneurial premium.

Sovereign Balance Sheets: Lendermarket

Lendermarket provides access to high-yield digital consumer loans sourced from massive international loan originators (such as Creditstar), frequently showcasing Average Annual Returns (AAR) of 15.58% in 2026.

The structural ceiling here lies within the mechanics of the Buyback Guarantee. Retail investors treat the buyback guarantee as a risk-free insurance policy. In truth, a buyback guarantee is not backed by a central bank or government insurance; it is merely a corporate promise. The guarantee is only as resilient as the standalone balance sheet of the loan originator. If a massive originator faces a systemic liquidity crunch, the guarantee collapses, revealing that your high yield was directly tied to institutional insolvency risk.

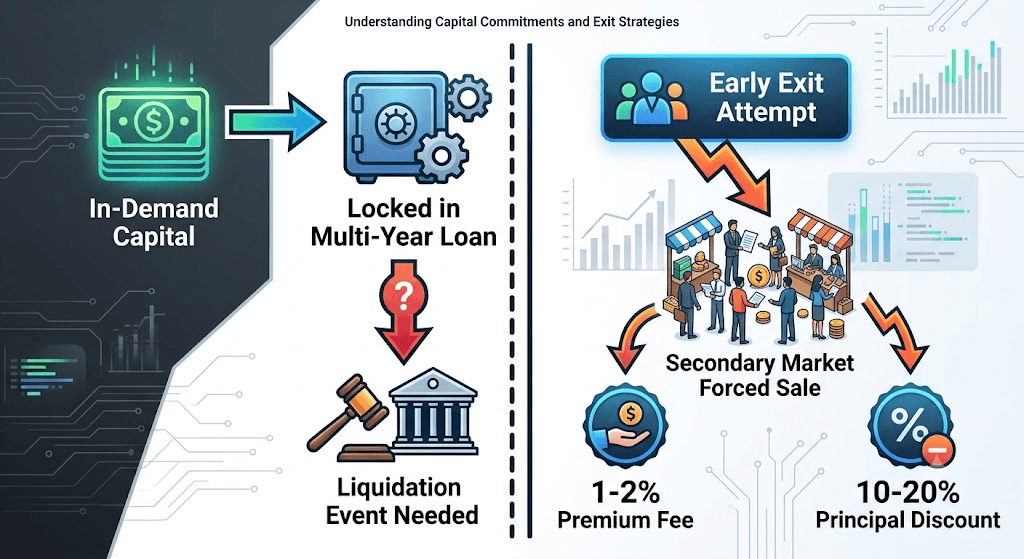

3. The Liquidity Trap: The Uncompromising “Time” Limit

The most profound hidden tax on your crowdfunding ROI is not defaults or platform fees—it is Time. Unlike trading equities on the New York Stock Exchange or London Stock Exchange, where you can instantly liquidate positions at 10:00 AM with a fraction of a penny in friction, crowdfunding assets are inherently, deeply illiquid.

If you deploy $50,000 into a 5-year peer-to-peer commercial development loan on a platform like Funding Circle, your capital is locked into that specific physical project. If an emergency arises and you require immediate capital preservation, your only escape hatch is the platform’s Secondary Market.

To exit early, you must list your loan notes at a discount to entice other buyers. In 2026, alternative platforms routinely charge a 1% to 2% transactional fee simply to utilize the secondary marketplace. Furthermore, if the loan shows any signs of stress, you may have to discount your principal by 10% to 20% to exit the position. This “Liquidity Tax” can instantly wipe out multiple years of accumulated interest payments in a single transaction.

4. Regulatory Frameworks: The Cost of “Skin in the Game.”

The implementation of European Crowdfunding Service Providers (ECSP) regulations and parallel SEC updates in the United States have drastically elevated consumer safety, but they have simultaneously functioned as a drag on retail ROI.

Under modern compliance rules, platforms like Indemo and Mintos mandate that loan originators retain an explicit “Skin in the Game” piece—typically keeping 5% to 10% of every single loan pool on their own corporate balance sheets. While this aligns incentives perfectly (ensuring originators don’t issue reckless loans), it alters the economics of the platform. Because the originators are retaining a portion of the debt, they naturally claim the safest, highest-yielding “top tier” tranches of the interest rate structure for themselves, distributing the lower-yielding, residual tiers to the retail public.

5. Institutional Crowding Out: The Leftover Problem

The final limit on your crowdfunding ROI is the entry of institutional sharks. What began a decade ago as a grassroots, peer-to-peer ecosystem for individual lenders has been entirely financialized. Today, multi-billion-dollar hedge funds, asset managers, and pension funds have integrated directly into alternative lending platforms via institutional API pipelines.

These institutional giants deploy high-speed, programmatic algorithms that scan every loan the millisecond it is uploaded to a platform like LendingClub or Zopa. The algorithms instantly “cherry-pick” the prime loans—those possessing the absolute highest credit scores, perfect LTV ratios, and optimized historical risk-adjusted metrics. By the time a retail investor manually logs into their dashboard, they are looking at the institutional “leftovers”—loans that carry either suppressed interest rates or elevated risk profiles. This continuous institutional crowding out has degraded average retail P2P net yields by an estimated 1.5% over the last three years.

6. How to Build an Uncapped Income Engine

If crowdfunding has structural caps, how do you build an asset base with genuine, unlimited upside? You shift a portion of your capital away from fixed-interest alternative debt platforms and move it into platforms that offer true, fractionalized, compounding equity ownership.

Two distinct alternatives allow you to bypass the structural limits of P2P debt:

Real Estate Equity Freedom: Lofty

If you want to escape the fixed-rate ceiling of real estate debt platforms like EstateGuru, Lofty offers a highly optimized alternative. Instead of lending money to a developer for a fixed 10% return, Lofty allows you to buy direct, tokenized equity fractions of cash-flowing U.S. rental properties starting at just $50.

Because you own the actual underlying equity, your income is completely uncapped. When the local real estate market appreciates, your token values rise dynamically. When rents increase due to inflation, your automated, daily rental distributions increase alongside them. Lofty elegantly combines the high yields of direct real estate with the instant liquidity of an active secondary marketplace, removing the classic “Time Limit” trap that plagues traditional crowdfunding.

Institutional Rental Aggregation: Fintown

For those seeking exposure to the thriving European real estate market without the volatility of developmental debt, Fintown provides a highly specialized direct-yield alternative. Powered by the veteran Vihorev Group, Fintown lets investors step directly into the lucrative short-term and corporate rental apartment market in prime tourist hubs like Prague.

Unlike developmental crowdfunding platforms, where your money is completely non-productive until a building is constructed, Fintown places your capital directly into already-existing, fully operational, income-generating premium properties. The platform yields between 9% and 12% annually, boasts an impressive 20% sponsor skin-in-the-game commitment to maximize safety, and crucially features a flexible “Flexi” product architecture that allows for daily interest accumulation and flexible early withdrawals—completely neutralizing the standard liquidity traps seen elsewhere in the P2P space.

Conclusion: Intentional Allocation

Crowdfunding and alternative P2P platforms deserve a functional home in a modern, diversified portfolio, but you must enter the arena with open eyes. The advertised 15% yields are raw figures that will inevitably be trimmed down by defaults, regulatory compliance costs, and institutional competition.

If your objective is fixed, passive income with defined collateral parameters, asset-backed debt platforms are excellent tools. But if your goal is true wealth amplification, you must avoid the fixed-debt ceiling. Transitioning your capital toward automated, equity-backed fractional real estate vehicles like Lofty or cash-flowing European rental assets via Fintown ensures that your long-term financial growth remains tied to real-world asset compounding, rather than a restricted, fixed-interest spreadsheet promise.

FAQ

What is the “Indemo Bonus” currently discussed in 2026?

To accelerate growth and expand market share, Indemo recently initiated a targeted promotional campaign offering structured cashback bonuses ranging from 2.5% to 5% for all net-new capital deployments exceeding €250, aiming to firmly cross its strategic target of 10,000 highly active retail platform investors before the end of the fiscal year.

Is P2P lending safer than keeping my cash in a traditional bank?

Absolutely not. A traditional bank deposit represents a regulated liability of a banking institution, heavily insulated by national government-backed guarantee schemes (such as the FDIC in the United States or national DGS frameworks across the European Union up to €100,000). A crowdfunding or P2P investment is a direct, speculative credit extension to a private borrower. If that borrower or the underlying platform faces insolvency, there is zero sovereign safety net to bail you out.

What does “Impermanent Loss” mean within the context of crowdfunding?

In alternative debt markets, impermanent loss (or opportunity cost friction) occurs when you lock your liquid capital into a multi-year, fixed-rate debt instrument yielding 10%, only to watch macro-economic inflation or central bank interest rates climb to 12%. Your capital is contractually trapped in an underperforming asset, actively losing real purchasing power despite technically booked nominal gains.

Which alternative platforms currently boast the highest historical recovery rates?

Historically, asset-backed real estate crowdfunding platforms like EstateGuru, Indemo, and Fintown maintain substantially higher capital recovery rates than consumer lending networks. This structural resilience exists because their loans are secured by a first-rank physical mortgage or direct ownership of underlying commercial/residential real estate, providing tangible hard assets that can be legally liquidated to make lenders whole during default scenarios.

Should I use the Auto-Invest tools provided by crowdfunding platforms?

While Auto-Invest algorithms offer extreme convenience and eliminate manual portfolio maintenance, in 2026, sophisticated high-net-worth investors still lean toward manual selection for concentrated portfolios. Manual curation allows you to closely inspect underlying LTVs, developer track records, and localized asset traits, completely insulating your capital from the automated “leftover drag” driven by high-speed institutional algorithms.